It’s not always easy to hold for the long term. Emotions often get in the way, resulting in counterintuitive short term thinking. Here are some guidelines to protect and growth your capital.

It’s not always easy to hold for the long term. Emotions often get in the way, resulting in counterintuitive short term thinking. Here are some guidelines to protect and growth your capital.

KEY TAKEAWAYS

- Behaviour surrounding the investments you own is more important than the investment vehicles themselves.

- The best way to combat the desire to make purely emotional decisions is to have a simple strategy with clear rules

- While “staying the course” is often the correct strategy, we seek to address the question, “what are the consequences if it is not the correct strategy”?

- By having a system in place to protect capital you can eliminate the large draw-downs which are more likely if you strictly “stay the course”.

- When protecting capital is of utmost concern having measures that allow for systematic unemotional decisions can lead to better long-term results

What does volatility mean to you?

Building a nest egg for the future has two components to it, the investments held in your portfolio and the behaviour surrounding your investment decisions. While investments are measured, analyzed, compared, and rationalized based on various quantifiable factors, the behaviour surrounding portfolio decisions is often ignored. Emotions are hard to quantify and summarize on a spreadsheet, however, ignoring this aspect can lead to suboptimal long-term results. The best way to combat the desire to make purely emotional decisions is to have a simple and intuitive strategy with clear rules.

Defining how you relate to the day to day market fluctuations can have an impact on your long term investment plan. Investing is an interesting journey, it elicits a range of continually changing emotions ranging from excitement to fear, optimism to pessimism, and complacency to action. Volatility can mean something different to everyone; to some it means loss of capital, to others it is seen as an uncomfortable fluctuation in the value of their nest egg, while a select few see it as an opportunity. Regardless of how you relate to market volatility it is wise to have a proactive approach in place to deal with it.

The Challenge

Subjecting your portfolio to large swings in value without a concrete plan often causes reactionary decisions that are made on a whim. These decisions are commonly made at inopportune times when the losses are large and there is no choice left but to reduce risk by liquidating positions. Volatility often persists for longer than expected and the inability to stick to a rules based approach can result in extended periods of time before recovering the value of your portfolio.

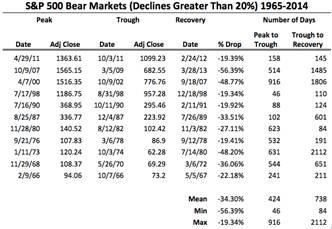

Source: McGraw Hill Financial

As the chart above shows (using the S&P 500) the average drop during market corrections is 34.3% once the markets decline by 20%, with an average time to recover of 1,178 days. That means on average during these market corrections you can experience periods of 3.2 years and time frames as long as 8.29 years with no return. By having a proactive plan in place and eliminating losses before they cross the 20% level increases your chances of protecting portfolio value and recovering losses in a shorter amount of time.

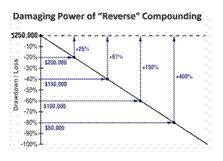

Figure 1 InvestTech Research

As this example demonstrates (based on an initial investment of $250,000) a decline of 20% requires a gain of 25% to get back to even, while a drop of -40% requiring a gain of 67% just to get back to your initial investment. The “law of reverse compounding” shows the difficultly in recovering if you don’t have a plan to deal with losses, as you have less money working, thus requiring a greater return on a smaller pool of capital. The number becomes even more daunting when drawing capital from your portfolio (ie. to support retirement income, to pay for expenses over and above your employment income) as you are forced to sell at lower prices leaving even less capital to generate returns. The path to your destination matters, especially as you get closer to relying on your savings for retirement.

What to do?

While “staying the course” is often the correct strategy, we seek to address the question, “what are the consequences if it’s not the correct strategy”?

We believe there is a better way to avoid these situations; having rules and risk controls in place to systematically remove capital from the market (keep in cash) at pre-determined levels once key barriers are broken. By having a system in place to protect capital you can eliminate the large draw-downs which are more likely if you strictly “stay the course”. When protecting capital is of utmost concern having measures that allow for systematic unemotional decisions can lead to better long-term results.

Here are a few tried and true rules when it comes to successful investing (in no particular order).

- Always use a investing plan (know when to hold em’, fold em’ and walk away!)

- Let your winners run and cut the losing positions

- Protect your capital

- Always have a stop loss (i.e. an exit plan)

- Don’t get emotionally attached to an investment

- No set of rules will work 100%, but can produce great results over time

- Simplicity in rules demonstrates wisdom. Complexity is a sign of inexperience.

- The best time to increase portfolio values is when a trend is present

- Lower your risk until you sleep well at night

- The markets cannot be predicted with certainty, understand how to play the probabilities.

In sports it is often said that the best offense is a good defense, the same applies to investing. Having a proactive approach to deal with the volatility affecting your portfolio can increase your odds of making rational decisions and ultimately helping you achieve your long term goals.

The views of Ryan Gerstel (Gerstel Wealth Management) do not necessarily reflect those of CIBC World Markets Inc. Clients are advised to seek advice regarding their particular circumstances from their personal tax and legal advisors. This information, including any opinion, is based on various sources believed to be reliable, but its accuracy cannot be guaranteed and is subject to change. CIBC Wood Gundy is a division of CIBC World Markets Inc., a subsidiary of CIBC and a Member of the Canadian Investor Protection Fund and Investment Industry Regulatory Organization of Canada. If you are currently a CIBC Wood Gundy client, please contact your Investment Advisor.